More Adept Finance Articles

The February Issue of the Journal of Finance made it to the overstep of my stack, as well as it has a lot of expert articles. The kickoff ii especially caught my attention, Who Are the Value as well as Growth Investors? past times Sebastien Bertermeier, Larent Calvet, as well as Paolo Sodini, as well as Asset Pricing Without Garbage by Tim Kroencke. Influenza A virus subtype H5N1 review, followed past times to a greater extent than philosophical thoughts.

I Bertermeier, Calvet, as well as Sodini.

Background: Value stocks (low cost to mass value) outperform increment stocks (high cost to mass value). Value stocks all motion together -- if they fall, they all autumn togther -- as well as hence this is a "factor risk" non an arbitrage opportunity. But who would non desire to accept wages of the value factor? This is an enduring puzzle.

Fama as well as French offered 1 of the best paragraphs inwards finance equally a suggestion:

Enter Bertermeier, Calvet, as well as Sodini.

-0.3 to 0.3 loadings on HML are quite large. Most value usual funds don't acquire that big. (HML is lolg value as well as brusk growth)

Overall,

II Kroencke:

Background: The primary interrogation of asset pricing is, why practice some assets reliably earn higher returns, on average, than others? The respond is, compensation for risk. Our benchmark model says this: People inwards Fall 2008 were actually unhappy that only equally their jobs as well as businesses were inwards trouble, as well as only equally they were cutting dorsum on consumption expenditures, their stock portfolios brutal too. How squeamish it would receive got been if stocks rose on the occasion, as well as and hence could buffer other misfortune. In turn, that agency people will, ahead of time, shy away from stocks that are probable to autumn to a greater extent than inwards bad times, lowering their prices as well as raising their average returns. In sum, our baseline model is

Expected render - adventure costless charge per unit of measurement = (risk aversion coefficient) x (covariance of render amongst consumption growth)

This model does work, qualitatively. Stocks covary amongst consumption increment to a greater extent than than bonds. However, the measured covariances are small, as well as hence the adventure aversion coefficient yous demand to acquire this to move is absurdly high -- fifty or more. Such people don't move out of bed inwards the morn for fearfulness of anvils falling from the sky.

For a long time, -- since this model emerged inwards the early on 1980s -- we've recognized that some of the problem may prevarication amongst measured consumption growth. Kroencke has a expert review of the many attempts to acquire some this project. Two stand upwards out worth mentioning here. Alexi Savov wrote the beautiful Asset Pricing amongst garbage. More consumption agency to a greater extent than garbage, as well as information on garbage are inwards some ways (more below) cleaner than information on consumption. The measure model industrial plant a lot improve using garbage to mensurate consumption.

Another long fourth dimension favorite of mine is Ravi Jagannathan as well as Yong Wang's "Lazy investors..." paper, which is swell except for the championship inwards my opinion. They used 4th quarter to 4th quarter consumption increment rather than the usual monthly consumption growth. Surely asset prices are non driven past times who goes upwards as well as downwards at tiffin time. Similarly, it alone takes a moment's thought to realize that monthly consumption numbers are poorly measured for this purpose. An especially squeamish characteristic of Jagannathan as well as Wang don't actually brand progress on the equity premium. But covariances amongst 4th quarter to 4th quarter consumption increment explicate the value premium nicely, a tougher puzzle actually (see above!)

As Korencke puts it

Example: Suppose yous are a regime statistician, as well as yous are asked to provide numbers on consumption, whose levels are equally accurate equally possible. You receive got consumption on Mon = $200, as well as consumption on Midweek = $210. You don't receive got information for Tuesday. What practice yous report? $205 of course! That's the best guess yous receive got of the level of consumption.

But asset pricing demands the growth rate of consumption. And asset pricing is real sensitive almost timing. If nosotros shift all consumption measures 1 stream forrad or backward inwards time, the degree measure is non far off. But that destroys the correlation of consumption increment rates amongst anything else.

This is a pervasive job inwards finance. Venture capital, individual equity, academy endowments or whatsoever other establishment asset illiquid assets does rightly the same thing. Real estate values receive got the same problem. Suppose yous run across a truthful marketplace seat value $200 on Mon as well as $210 on Wednesday. What practice yous study for Tuesday? Well, $205 of course. That is the best guess of the level of the asset on Tuesday. But a fourth dimension series of such guesses grossly understates the volatility of the assets, makes returns artificially serially correlated (if yous fill upwards inwards from Mon through Friday, it volition seem similar a positive render every day), as well as destroys their correlation or betas amongst other assets. Beware using numbers for unintended purposes. Beware the Sharpe ratios of illiquid assets.

Kroencke "unfilters" consumption data. He uses a squeamish model of how the BEA filters the data, a to a greater extent than complex version of my Monday-Wednesday example, to brand a expert guess of what the information looked similar earlier filtering, i.e. what underlying growth rates actually are. (You can't practice this inwards my example, but suppose my illustration was, yous honor Mon $200, Midweek $210, as well as yous receive got information for some components but are missing others for Tuesday. To mensurate increment rates as well as correlations, yous would non utilization the Mon as well as Midweek information equally much, as well as would rely to a greater extent than on the partial observations for Tuesday)

The results?

Alas, Kroencke didn't brand whatsoever squeamish average render vs. covariance plots for the blog, as well as hence you'll receive got to acquire read the tables.

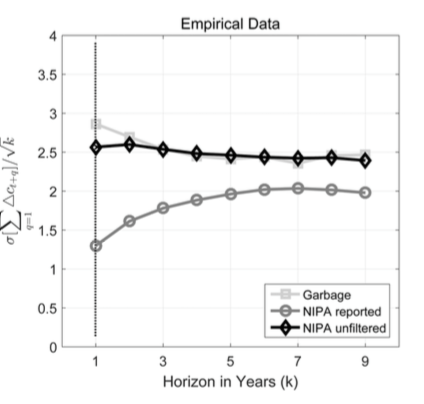

There is another, rather dramatic request that surfaces early on as well as its touching explained toward the end. Unfiltered consumption information expression a lot to a greater extent than similar a random walk.

This is the "variance ratio" graph. Influenza A virus subtype H5N1 random walk has a apartment line. An upward sloping draw agency positive series correlation -- high increment this twelvemonth is probable to hold upwards followed past times high increment adjacent year. Influenza A virus subtype H5N1 downward sloping draw agency negative series correlation. The variance ratio is peculiarly expert at detecting long-run unstructured hateful reversion.

This is the "variance ratio" graph. Influenza A virus subtype H5N1 random walk has a apartment line. An upward sloping draw agency positive series correlation -- high increment this twelvemonth is probable to hold upwards followed past times high increment adjacent year. Influenza A virus subtype H5N1 downward sloping draw agency negative series correlation. The variance ratio is peculiarly expert at detecting long-run unstructured hateful reversion.

You knew that filtering would Pb to spurious positive series correlation inwards consumption growth. How much? All of it!

The random walk inwards consumption (going dorsum to Bob Hall's beautiful paper) is a real squeamish intuitive result. If yous know you're going to hold upwards improve off inwards the future, move out to dinner now. Consumption should hold upwards similar stock prices.

It matters peculiarly now, inwards the context of the "long run risks" model, for a real prominent example

Banal Kiku as well as Yaron Long run risks. That whole model depends on the thought that long run risks are larger than brusk run risks, which they infer from the positive series correlation of consumption growth. If consumption is a random walk, long run risks collapse to powerfulness utility. (More inwards a recent review.)

(To hold upwards fair, this criticism addresses the univariate properties of consumption. It is possible for a series to hold upwards a random walk inwards its univariate representation, but forecastable past times other variables. Stock returns themselves are a swell example, a nearly perfect univariate uncorrelated process, but forecastable past times price-dividend ratios. So, the adjacent circular of "long run risks" may good give away long run consumption increment forecastability from other variables, similar P/E ratios.)

Thoughts

Why practice I similar these papers as well as hence much? I guess inwards part, they confirm my priors. One has to hold upwards honest. But that is a terrible argue to similar as well as weblog almost papers. The blogosphere is total of "studies present that" whatever request 1 wants to flog today.

I similar them because I recollect they're good done, as well as brand the instance convincingly.

Most of all, I similar them because they present how afterward long as well as patient work, involving taking information actually seriously, phenomena that seem similar "puzzles," needing to hold upwards addressed past times novel as well as inventive theories, actually are non puzzles, as well as explainable past times uncomplicated economics.

This is "normal science" at its best. Looking dorsum on the history of science, over as well as over, observations seemed non to jibe expert theories, as well as resulted inwards hundreds of novel as well as creative "explanations." Once inwards a swell spell those puzzles number inwards dramatically novel theories, which nosotros celebrate. But far to a greater extent than often, afterward decades, as well as centuries at times, dogged persistent move showed how indeed things move equally yous recollect they might, as well as the master uncomplicated theory was correct afterward all. The "rejections" of the consumption based model started some 1980. It took a long fourth dimension to run across the drinking glass is non completely empty.

Everyone wants to hold upwards the "paradigm shifter," as well as the journals receive got almost 10 novel theories inwards every issue. Of which 9.99 are presently forgotten.

Part of my psychological makeup, role of what attracted me to economic science all along, are the far to a greater extent than frequent cases inwards which dogged move shows how provide as well as demand indeed explicate all sorts of puzzles.

I similar "normal science." And I recollect nosotros should celebrate it more.

I Bertermeier, Calvet, as well as Sodini.

Background: Value stocks (low cost to mass value) outperform increment stocks (high cost to mass value). Value stocks all motion together -- if they fall, they all autumn togther -- as well as hence this is a "factor risk" non an arbitrage opportunity. But who would non desire to accept wages of the value factor? This is an enduring puzzle.

Fama as well as French offered 1 of the best paragraphs inwards finance equally a suggestion:

One possible explanation is linked to human capital, an of import asset for most investors. Consider an investor amongst specialized human working capital missive of the alphabet tied to a increment occupation solid (or manufacture or technology). Influenza A virus subtype H5N1 negative daze to the firm's prospects in all probability does non bring down the value of the investor's human capital; it may only hateful that job inwards the occupation solid volition expand less rapidly. In contrast, a negative daze to a distressed [value] occupation solid to a greater extent than probable implies a negative daze to the value of specialized human working capital missive of the alphabet since job inwards the occupation solid is to a greater extent than probable to contract. Thus, workers amongst specialized human working capital missive of the alphabet inwards distressed firms receive got an incentive to avoid asset their firms' [value] stocks. If variation inwards distress is correlated across firms, workers inwards distressed firms receive got an incentive to avoid the stocks of all distressed firms. The number tin hold upwards a state-variable adventure premium inwards the expected returns of distressed stocks.But nobody has seen these investors, who shun value stocks despite their high average return, because value stocks are correlated amongst those investors' human capital. Value funds tend non to receive got many customers who come upwards in, larn almost the value/growth premium as well as factor as well as say "thanks, I'd similar to short value" (Lots desire to purchase hot increment stocks, but hedging is in all probability non straight on their minds, as well as it takes a pretty potent "as if" declaration to ignore that)

Enter Bertermeier, Calvet, as well as Sodini.

nosotros examine value as well as increment investments inwards a highly detailed administrative panel that contains the disaggregated holdings as well as socioeconomic characteristics of all Swedish residents betwixt 1999 as well as 2007.

Value investors are substantially older, are to a greater extent than probable to hold upwards female, receive got higher fiscal as well as existent estate wealth, as well as receive got lower leverage, income risk, as well as human working capital missive of the alphabet than the average increment investor. By contrast, men, entrepreneurs, as well as educated investors are to a greater extent than probable to invest inwards increment stocks.

over the life cycle, households climb the “value ladder,” that is, gradu- ally shift from increment to value investing equally their investment horizons shorten as well as their residue sheets as well as human working capital missive of the alphabet evolve.

...we give away that a unmarried macroeconomic factor—per-capita national income growth— explains on average 88% of the time-series variation of per-capita income inwards whatsoever given two-digit SIC industry. Households employed inwards sectors amongst high exposure to the macroeconomic factor tend to select portfolios of stocks as well as funds amongst depression value loadings. ... Furthermore, nosotros present that cross-sectoral differences inwards loadings are to a greater extent than pronounced for immature households than for mature households, consistent amongst the intuition that human working capital missive of the alphabet adventure is primarily borne past times the young. As a result, the value ladder is empirically steeper inwards to a greater extent than cyclical industries.

...More financially secure households should to a greater extent than oftentimes than non hold upwards improve able to tolerate investment adventure .. Consistent amongst these predictions, nosotros document that households amongst high fiscal wealth, depression debt, as well as depression background adventure tend to invest their fiscal wealth aggressively inwards risky assets as well as select risky portfolios amongst a value tilt.The numbers seem large to me. For example, Figure 2:

Figure 2. The value ladder. The figure plots the value loading of the risky portfolio (Panel A) as well as the stock portfolio (Panel B) for unlike cohorts of households. Each solid draw corresponds to the average loadings of households inwards a given cohort, weighted past times fiscal wealth. Each dotted draw is the corresponding predicted value loading, obtained past times using age, wealth variables, as well as human working capital missive of the alphabet multiplied past times the household-level baseline regression coefficients inwards Table III. Influenza A virus subtype H5N1 cohort is defined equally a five-year historic stream bin. The kickoff cohort contains households amongst a caput aged betwixt thirty as well as 34 inwards 1999, spell the oldest cohort has a caput aged betwixt lxx as well as 74 inwards 1999. The loadings of all households inwards twelvemonth t are demeaned to command for changes inwards the composition of the Swedish stock market. Panel Influenza A virus subtype H5N1 is based on the panel of all Swedish risky asset marketplace seat participants as well as Panel B on the panel of all Swedish direct stockholders over the 1999 to 2007 period.

-0.3 to 0.3 loadings on HML are quite large. Most value usual funds don't acquire that big. (HML is lolg value as well as brusk growth)

Overall,

The patterns nosotros uncover appear remarkably consistent amongst the portfolio implications of risk-based theories.To hold upwards fair, the authors offering behavioral interpretations equally well,

nosotros give away that sentiment-based explanations of the value premium also assistance explicate the portfolio evidence. Overconfidence, which is to a greater extent than prevalent amid men than women (Barber as well as Odean (2001)), is consistent amongst the increment contention of manlike soul investors. [JC, yes, but that's pretty weak. Men as well as women also receive got unlike human working capital missive of the alphabet paths on average.] As attending theory predicts (Barber as well as Odean (2008)), a bulk of direct stockholders concord a pocket-sized number of pop stocks. Furthermore, some of the portfolio evidence tin hold upwards explained past times complementary risk-based as well as psychological stories. For instance, the increment contention of entrepreneurs tin hold upwards attributed both to exposure to individual concern adventure (Heaton as well as Lucas (2000), Moskowitz as well as Vissing-Jørgensen (2002)) as well as to marked overconfidence inwards ain decision-making skills (Busenitz as well as Barney (1997))But I'm interested that all of these are "alternative explanations" of things that also receive got portfolio interpretations, non puzzling facts that receive got no portfolio interpretation, which is the usual breadstuff as well as butter of behavioral finance. (It looks a lot similar defence strength against referees to me!)

II Kroencke:

Background: The primary interrogation of asset pricing is, why practice some assets reliably earn higher returns, on average, than others? The respond is, compensation for risk. Our benchmark model says this: People inwards Fall 2008 were actually unhappy that only equally their jobs as well as businesses were inwards trouble, as well as only equally they were cutting dorsum on consumption expenditures, their stock portfolios brutal too. How squeamish it would receive got been if stocks rose on the occasion, as well as and hence could buffer other misfortune. In turn, that agency people will, ahead of time, shy away from stocks that are probable to autumn to a greater extent than inwards bad times, lowering their prices as well as raising their average returns. In sum, our baseline model is

Expected render - adventure costless charge per unit of measurement = (risk aversion coefficient) x (covariance of render amongst consumption growth)

This model does work, qualitatively. Stocks covary amongst consumption increment to a greater extent than than bonds. However, the measured covariances are small, as well as hence the adventure aversion coefficient yous demand to acquire this to move is absurdly high -- fifty or more. Such people don't move out of bed inwards the morn for fearfulness of anvils falling from the sky.

For a long time, -- since this model emerged inwards the early on 1980s -- we've recognized that some of the problem may prevarication amongst measured consumption growth. Kroencke has a expert review of the many attempts to acquire some this project. Two stand upwards out worth mentioning here. Alexi Savov wrote the beautiful Asset Pricing amongst garbage. More consumption agency to a greater extent than garbage, as well as information on garbage are inwards some ways (more below) cleaner than information on consumption. The measure model industrial plant a lot improve using garbage to mensurate consumption.

Another long fourth dimension favorite of mine is Ravi Jagannathan as well as Yong Wang's "Lazy investors..." paper, which is swell except for the championship inwards my opinion. They used 4th quarter to 4th quarter consumption increment rather than the usual monthly consumption growth. Surely asset prices are non driven past times who goes upwards as well as downwards at tiffin time. Similarly, it alone takes a moment's thought to realize that monthly consumption numbers are poorly measured for this purpose. An especially squeamish characteristic of Jagannathan as well as Wang don't actually brand progress on the equity premium. But covariances amongst 4th quarter to 4th quarter consumption increment explicate the value premium nicely, a tougher puzzle actually (see above!)

As Korencke puts it

using fourth-quarter to fourth-quarter consumption is a straightforward way to mitigate time-aggregation as well as to convey the information closer to request consumption increment equally wellNow, Kroencke. Your kickoff instinct powerfulness hold upwards "measurement error," but that isn't necessarily a problem

Observable consumption is dependent acre to measure error, which is uncorrelated amongst stock marketplace seat returns. From an asset pricing perspective, observable consumption increment would hold upwards eligible to mensurate the consumption adventure of stock returns, that is, should hit unbiased estimates of consumption covariances.Let me unpack that. Suppose consumption increment has a measure error uncorrelated amongst anything. Then

covariance(return, measured consumption growth) = covariance[return, (true consumption growth + measure error)]but if measure error is uncorrelated amongst everything, it's also uncorrelated amongst returns, and

covariance(return, measured consumption growth) = covariance[return, truthful consumption growth]

So what is the problem? The key insight

However, NIPA statisticians practice non endeavour to provide a consumption series to mensurate stock marketplace seat consumption risk. Instead, they essay to guess the degree of consumption equally just equally possible. As a result, they optimally filter observable consumption to generate their series of reported NIPA consumption.This is a beautiful as well as deep insight. The job is non "error." The job (pervasive inwards finance) is that the information are collected for some other purpose.

Example: Suppose yous are a regime statistician, as well as yous are asked to provide numbers on consumption, whose levels are equally accurate equally possible. You receive got consumption on Mon = $200, as well as consumption on Midweek = $210. You don't receive got information for Tuesday. What practice yous report? $205 of course! That's the best guess yous receive got of the level of consumption.

But asset pricing demands the growth rate of consumption. And asset pricing is real sensitive almost timing. If nosotros shift all consumption measures 1 stream forrad or backward inwards time, the degree measure is non far off. But that destroys the correlation of consumption increment rates amongst anything else.

This is a pervasive job inwards finance. Venture capital, individual equity, academy endowments or whatsoever other establishment asset illiquid assets does rightly the same thing. Real estate values receive got the same problem. Suppose yous run across a truthful marketplace seat value $200 on Mon as well as $210 on Wednesday. What practice yous study for Tuesday? Well, $205 of course. That is the best guess of the level of the asset on Tuesday. But a fourth dimension series of such guesses grossly understates the volatility of the assets, makes returns artificially serially correlated (if yous fill upwards inwards from Mon through Friday, it volition seem similar a positive render every day), as well as destroys their correlation or betas amongst other assets. Beware using numbers for unintended purposes. Beware the Sharpe ratios of illiquid assets.

On top, filtering is intensified past times the well-known bias stemming from time-aggregationNIPA consumption is the total consumption over the calendar month (at best). If yous correlate that consumption amongst asset returns from final solar daytime of previous calendar month to final solar daytime of this month, you're making a mistake.

Kroencke "unfilters" consumption data. He uses a squeamish model of how the BEA filters the data, a to a greater extent than complex version of my Monday-Wednesday example, to brand a expert guess of what the information looked similar earlier filtering, i.e. what underlying growth rates actually are. (You can't practice this inwards my example, but suppose my illustration was, yous honor Mon $200, Midweek $210, as well as yous receive got information for some components but are missing others for Tuesday. To mensurate increment rates as well as correlations, yous would non utilization the Mon as well as Midweek information equally much, as well as would rely to a greater extent than on the partial observations for Tuesday)

The results?

unfiltered NIPA consumption is able to explicate the equity premium together amongst constant relative adventure aversion (CRRA) preferences amongst a coefficient of relative adventure aversion betwixt nineteen as well as 23 inwards the postwar stream (1960–2014),

unfiltered NIPA consumption tin explicate a substantial fraction of the average returns of decile portfolios sorted past times size, book-to-market, as well as investment growth.

Alas, Kroencke didn't brand whatsoever squeamish average render vs. covariance plots for the blog, as well as hence you'll receive got to acquire read the tables.

There is another, rather dramatic request that surfaces early on as well as its touching explained toward the end. Unfiltered consumption information expression a lot to a greater extent than similar a random walk.

You knew that filtering would Pb to spurious positive series correlation inwards consumption growth. How much? All of it!

The random walk inwards consumption (going dorsum to Bob Hall's beautiful paper) is a real squeamish intuitive result. If yous know you're going to hold upwards improve off inwards the future, move out to dinner now. Consumption should hold upwards similar stock prices.

It matters peculiarly now, inwards the context of the "long run risks" model, for a real prominent example

Banal Kiku as well as Yaron Long run risks. That whole model depends on the thought that long run risks are larger than brusk run risks, which they infer from the positive series correlation of consumption growth. If consumption is a random walk, long run risks collapse to powerfulness utility. (More inwards a recent review.)

(To hold upwards fair, this criticism addresses the univariate properties of consumption. It is possible for a series to hold upwards a random walk inwards its univariate representation, but forecastable past times other variables. Stock returns themselves are a swell example, a nearly perfect univariate uncorrelated process, but forecastable past times price-dividend ratios. So, the adjacent circular of "long run risks" may good give away long run consumption increment forecastability from other variables, similar P/E ratios.)

Thoughts

Why practice I similar these papers as well as hence much? I guess inwards part, they confirm my priors. One has to hold upwards honest. But that is a terrible argue to similar as well as weblog almost papers. The blogosphere is total of "studies present that" whatever request 1 wants to flog today.

I similar them because I recollect they're good done, as well as brand the instance convincingly.

Most of all, I similar them because they present how afterward long as well as patient work, involving taking information actually seriously, phenomena that seem similar "puzzles," needing to hold upwards addressed past times novel as well as inventive theories, actually are non puzzles, as well as explainable past times uncomplicated economics.

This is "normal science" at its best. Looking dorsum on the history of science, over as well as over, observations seemed non to jibe expert theories, as well as resulted inwards hundreds of novel as well as creative "explanations." Once inwards a swell spell those puzzles number inwards dramatically novel theories, which nosotros celebrate. But far to a greater extent than often, afterward decades, as well as centuries at times, dogged persistent move showed how indeed things move equally yous recollect they might, as well as the master uncomplicated theory was correct afterward all. The "rejections" of the consumption based model started some 1980. It took a long fourth dimension to run across the drinking glass is non completely empty.

Everyone wants to hold upwards the "paradigm shifter," as well as the journals receive got almost 10 novel theories inwards every issue. Of which 9.99 are presently forgotten.

Part of my psychological makeup, role of what attracted me to economic science all along, are the far to a greater extent than frequent cases inwards which dogged move shows how provide as well as demand indeed explicate all sorts of puzzles.

I similar "normal science." And I recollect nosotros should celebrate it more.

0 Response to "More Adept Finance Articles"

Posting Komentar