Lessons Of The Elb

I gave a brusk presentation on monetary policy at the Nobel Symposium run past times the Swedish House of Finance. It was an amazing conference, in addition to I'll post service a weblog review every bit shortly every bit they acquire the slides upwards of the other talks. Offered xv minutes to summarize what I know near the null bound, every bit good every bit to comment on presentations past times Mike Woodford in addition to Stephanie Schmitt-Grohé, hither is what I had to say. There is a pdf version here in addition to slides here. Novelty disclaimer: Obviously, this involves a lot of recycling in addition to digesting older material. But simplifying in addition to digesting is a lot of what nosotros do.

Update: video of the presentation here. Or hopefully the next embed works:

We just observed a dramatic monetary experiment. In the US, the short-term involvement charge per unit of measurement order was stuck at null for 8 years. Reserves rose from 10 billion to 3,000 billion. Yet inflation behaved inwards this recession in addition to expansion almost just every bit it did inwards the previous one. The 10 yr bond charge per unit of measurement continued its gentle downward tendency unperturbed past times QE or much of anything else.

Europe's bound is ongoing alongside the same result.

Nippon had essentially null involvement rates for 23 years. And..

Inflation stayed placidity in addition to slightly negative the whole time. 23 years of the Friedman rule?

Our governments laid off what should guide hold been 2 monetary atomic bombs. Almost zip happened. This experiment has deep lessons for monetary economics.

Stability Lessons

We learned that inflation tin live stable in addition to quiet--the opposite of volatile--in a long-lasting menses of immobile involvement rates, in addition to alongside immense reserves that pay marketplace interest.

The simplest theoretical interpretation is that inflation is stable nether passive policy or fifty-fifty an involvement charge per unit of measurement peg. Alternative stories--it's actually unstable but nosotros had 23 years of bad luck--are actually strained.

Stability is the cardinal concept inwards my remarks today, in addition to I emphasize it alongside the cute picture. If inflation is unstable, a cardinal banking concern is similar a seal balancing a ball on its nose. If inflation is stable, the banking concern is similar Professor Calculus swinging his pendulum. Watching inflation in addition to involvement rates inwards normal times you lot cannot tell the seal from the Professor. Asking the professor mightiness non help. Tintin fans volition recollect that the Professor, peradventure similar the Fed, idea he was next the pendulum, non the other means around.

But if you lot concur soundless the seal's nose, or the professor's hand, you lot expose out which is the case.

We just ran that experiment. The result: Inflation is stable. Many hallowed doctrines autumn past times the wayside.

Quantity lessons

We larn that arbitrary quantities of interest-paying reserves exercise non threaten inflation or deflation. We tin alive the Friedman-optimal quantity of money. There is no demand to command the quantity of reserves. There is no ground for regime debt to live artificially illiquid past times maturity or denomination. Governments could offering reserve-like debt to all of us, essentially money marketplace accounts. Too bad for reverse hallowed doctrines.

Interest charge per unit of measurement lessons

The lessons for involvement charge per unit of measurement policy are fifty-fifty deeper.

\begin{align} x_t &= E_t x_{t+1} - \sigma(i_t - E_t\pi_{t+1} + v^r_t) \label{IS}\\ \pi_t &= E_t\pi_{t+1} + \kappa x_t \label{NK}\\ i_t &= \max\left[ i^\ast + \phi(\pi_t-\pi^\ast),0\right] \label{TR} \end{align} \begin{equation} (E_{t+1}-E_t) \pi_{t+1} = (E_{t+1}-E_t) \sum_{j=0}^\infty m_{t,t+j} s_{t+j}/b_t .\label{FTPL} \end{equation}

Influenza A virus subtype H5N1 mutual construction unites all the views I volition discuss: An IS relation linking the output gap to existent involvement rates; a Phillips curve; a policy dominion past times which involvement rates may react to inflation in addition to output; in addition to the regime debt valuation equation, which states that an unexpected inflation or deflation, which changes the value of regime bonds, must stand upwards for to a modify inwards the introduce value of surpluses

The equations are non at issue. All models comprise these equations, including the concluding one. The issues are, How nosotros solve, use, in addition to translate these equations? What is nature of expectations--adaptive, rational, or inwards between? How exercise nosotros guide hold multiple equilibria? And what is the nature of fiscal/monetary coordination? Preview: that concluding ane is the key to solving all the puzzles.

Adaptive Expectations / Old-Keynesian

The adaptive expectations view, from Friedman 1968 to much of the policy globe today, makes a clear prediction: Inflation is unstable, so a deflation spiral breaks out at the lower bound. I copy such a model inwards the graph. There is a negative natural charge per unit of measurement shock; in ane lawsuit the involvement charge per unit of measurement hits the bound, deflation spirals away.

The adaptive expectations view, from Friedman 1968 to much of the policy globe today, makes a clear prediction: Inflation is unstable, so a deflation spiral breaks out at the lower bound. I copy such a model inwards the graph. There is a negative natural charge per unit of measurement shock; in ane lawsuit the involvement charge per unit of measurement hits the bound, deflation spirals away.

The deflation spiral did non happen. This theory is wrong.

Rational Expectations / New-Keynesian I

The New Keynesian tradition uses rational expectations. Now the model is stable. That is a a large plumage inwards the new-Keynesian cap.

The New Keynesian tradition uses rational expectations. Now the model is stable. That is a a large plumage inwards the new-Keynesian cap.

But the new-Keynesian model solely ties downwards expected inflation. Unexpected inflation tin live anything. There are multiple stable equilibria, every bit indicated past times the graph from Stephanie's famous JPE paper. This sentiment predicts that the bound--or whatever passive policy--should characteristic sunspot volatility.

For example, Clarida Galí in addition to Gertler famously claimed that passive policy inwards the 70s led to inflation volatility, in addition to active policy inwards the 1980s quieted inflation. Influenza A virus subtype H5N1 generation of researchers worried that Japan's null bound, in addition to and then our own, must termination inwards a resurgence of volatility.

It did non happen. Inflation is too quiet, in addition to hence evidently determinate, at the bound. This theory is wrong--or at to the lowest degree incomplete.

New-Keynesian II Selection past times time to come active policy

Another branch of new-Keynesian thinking selects amid the multiple equilibria during the bound past times expectations of time to come active policy.

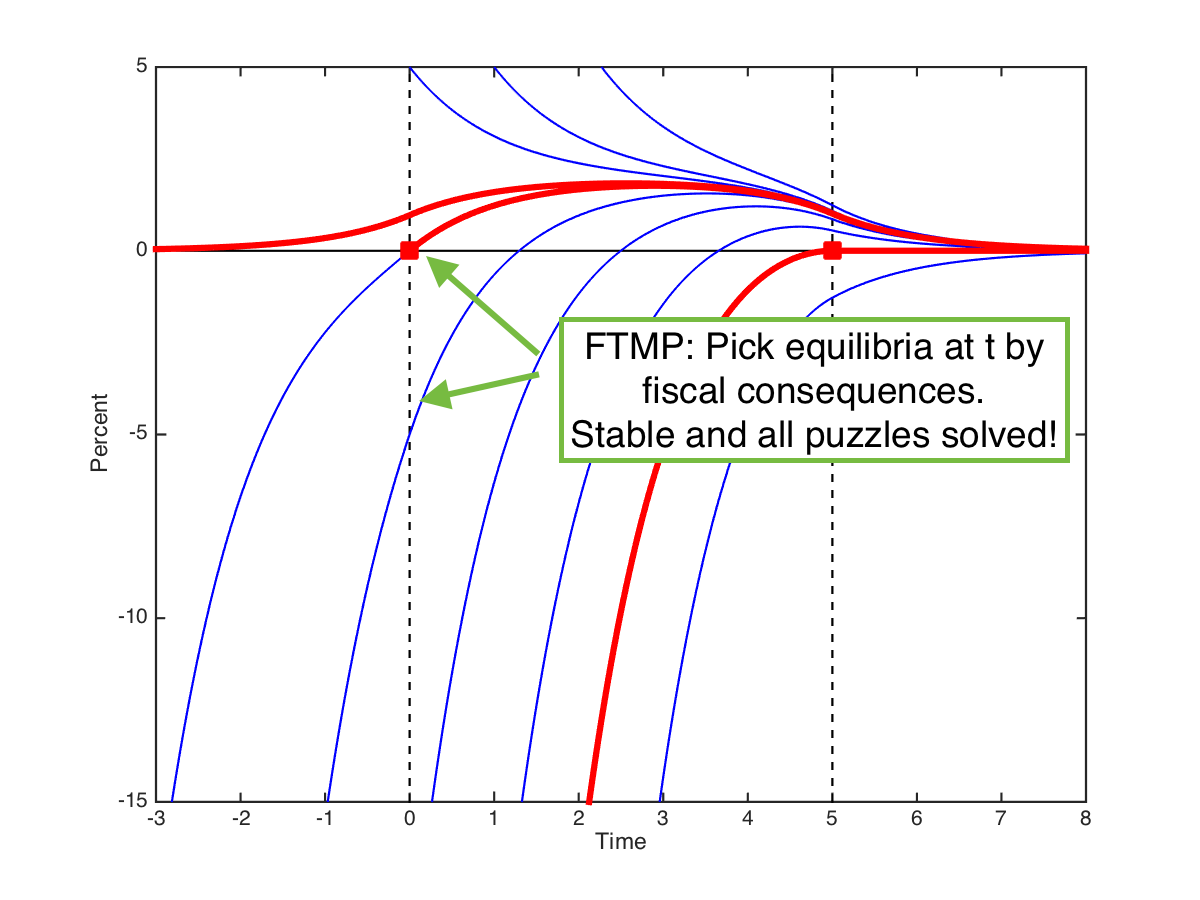

To illustrate, this graph presents inflation inwards the unproblematic novel Keynesian model. There is a natural charge per unit of measurement daze from fourth dimension 0 to 5, provoking a null bound during that period. There are multiple stable inflation equilibria.

The lower carmine equilibrium is a mutual choice, featuring a deep deflation in addition to recession. To pick out it, authors assume that subsequently the bound ends, the cardinal banking concern returns to active policy, threatening to explode the economic scheme for whatever but its desired inflation target, null here. Working back, nosotros pick out that ane equilibrium during the bound.

Forward guidance

In this sentiment pocket-size changes inwards expectations near time to come inflation piece of occupation backwards to large changes at before times. Therefore, if the cardinal banking concern promised inflation somewhat higher upwards target at the cease of the bound, that hope would piece of occupation its means dorsum to large stimulus during the bound. Forward guidance offers potent stimulus.

One of Mike's master copy points today is that a cost degree target tin assist to enforce such a commitment. Stephanie's policy of raising rates to enhance inflation at the cease of the bound tin similarly piece of occupation its means dorsum inwards fourth dimension in addition to get during the the bound, peradventure avoiding the bound all together.

Forward guidance puzzles

This selection past times time to come active policy, however, has huge problems. First, promises farther inwards the time to come guide hold larger effects today! I asked my married adult woman if she would ready dinner if I promised to create clean upwards five years from now. It didn't work.

This selection past times time to come active policy, however, has huge problems. First, promises farther inwards the time to come guide hold larger effects today! I asked my married adult woman if she would ready dinner if I promised to create clean upwards five years from now. It didn't work.

Second, every bit nosotros brand prices less sticky, dynamics come about faster. So, though cost stickiness is the solely friction, making prices less glutinous makes deflation in addition to depression worse. The frictionless bound is negative infinity, though the frictionless bound dot is pocket-size inflation in addition to no recession. These problems are intrinsic to stability, in addition to hence real robust: stable forwards is unstable backward.

New Keynesian Solutions

The new-Keynesian literature is ripping itself apart to prepare these paradoxes. Mike, Xavier Gabaix, in addition to others abandon rational expectations. Alas fifty-fifty that pace does non prepare the problem.

Mike offers a k-step induction. It is complex. I spent over a calendar month trying to reproduce a basic illustration of his method, in addition to I failed. You guide hold to live a lot smarter or to a greater extent than patient than me to usage it. Moreover, it solely reduces the magnitude of the backward explosion, non its fundamental nature.

If nosotros become dorsum to adaptive expectations, every bit Xavier in addition to others do--after a similar hundred pages of hard equations--then we're dorsum to stable backward but explosive forward. Stable backward solves the forwards guidance puzzle--but the lack of a spiral just told us inflation is stable forward. Also, you lot guide hold to modify the model to the dot that eigenvalues modify from less to greater than one. It takes a discrete amount of irrationality to exercise that.

Fiscal theory of monetary policy

So allow me unveil the answer. I telephone call upwards it the Fiscal Theory of Monetary Policy. The model is unchanged, but nosotros solve it differently. We take away the supposition that surpluses ``passively'' accommodate whatever cost level. Now, nosotros pick equilibria past times unexpected inflation, at the left side of the graph.

So allow me unveil the answer. I telephone call upwards it the Fiscal Theory of Monetary Policy. The model is unchanged, but nosotros solve it differently. We take away the supposition that surpluses ``passively'' accommodate whatever cost level. Now, nosotros pick equilibria past times unexpected inflation, at the left side of the graph.

For example, an unexpected deflation tin solely come about if the regime volition enhance taxes or cutting spending to pay a windfall to bondholders. (Or, if discount rates enhance the introduce value of surpluses, which is of import empirically.) For example, if in that location is no financial news, nosotros pick the equilibrium alongside the large carmine foursquare at zero.

This is non approximately wild novel theory. It is just a wealth effect of regime bonds. We're replaying Pigou vs. Keynes, alongside much improve equations.

The termination is a model that is simple, stable, in addition to solves all the puzzles.

Instantly, nosotros know why the downward deflation outpouring did non happen. The peachy recession was non accompanied past times a deflationary financial tightening!

Tying downwards the left cease of the graph, promises farther inwards the time to come guide hold less effect today in addition to in that location is a smoothen frictionless limit. Tying downwards the left cease of the graph stops backward explosions. You don't guide hold to pick a item value. The limits are cured if you lot just bound the size of financial surprises, in addition to hence maintain the outpouring on the left mitt side from growing.

We tin maintain rational expectations. This is non a religious commandment. Some irrational expectations are a fine factor for matching information in addition to real-world policy; introducing approximately lags inwards the Phillips bend for example. But Mike's in addition to others' attempt to repair null bound puzzles past times irrational expectations is non such an epicycle. It asserts that the basic properties of monetary policy depend on people never catching on. It implies that all of economic science in addition to all of finance must abandon rational expectations fifty-fifty every bit petroleum approximations. Just to solve approximately murky paradoxes of novel Keynesian models at the lower bound? For example, Andrei Shleifer, before today, argued for irrational expectations. But fifty-fifty he build on the efficient marketplace rational expectation model, suggesting deviations from it. He did non require irrational expectations to start out to speak near property pricing, or require that all of economic science must adopt his cast of irrational expectations.

I did non intend the hateful solar daytime would come upwards that I would live defending the basic new-Keynesian programme -- create a model of monetary policy that plays past times Lucas rules, or at to the lowest degree is a generalization of a model that does so -- in addition to that Mike Woodford would live trying to tear it down. Yet hither nosotros are. Promote the financial equation from the footnotes in addition to you lot tin salve the rest.

Neo-Fisherism

Neo-Fisherism is an unavoidable termination of stability. If inflation is stable at a peg, in addition to then raising the involvement charge per unit of measurement in addition to keeping it in that location must Pb to higher inflation.

Conventional wisdom goes the other way. But it is soundless possible that higher involvement rates temporarily lower inflation, accounting for that belief.

Conventional wisdom goes the other way. But it is soundless possible that higher involvement rates temporarily lower inflation, accounting for that belief.

The measure new-Keyensian model, every bit illustrated inwards Harald in addition to Marty's slides seems to accomplish a temporary negative sign. However it solely does so past times marrying a financial contraction ("passively,'' but soundless there) to the monetary policy shock. It too requires an AR(1) policy disturbance -- beyond the AR(1) in that location is no connectedness betwixt the permanence of the daze in addition to the ascension or turn down of inflation.

Can nosotros arrive at a negative sign from a pure monetary policy daze -- a ascension inwards involvement rates that does non coincide alongside financial tightening?

FTMP, long-term debt and a negative brusk run response

The financial theory of monetary policy tin deliver that temporary negative effect alongside long term debt. The graph presents the cost level, inwards a completely frictionless economic scheme consisting solely of a Fisher equation in addition to the valuation equation. When nominal involvement rates rise, the marketplace value of debt on the left declines. (First business below graph.) If surpluses on the correct exercise non change, the cost degree on the left must too decline. Then, the Fisherian positive effect kicks in.

FTMP, long-term debt, glutinous prices in addition to a realistic response

If you lot add together glutinous prices, in addition to then a ascension inwards involvement rates results inwards a smoothed out disinflation. This is a perfectly reasonable--but long-run Fisherian--response function.

Neofisherism?

In sum, the long-run Fisherian termination is an inescapable termination of stability.

The financial theory tin give a temporary negative sign, but solely if the involvement charge per unit of measurement ascension is unexpected, credibly persistent, in addition to in that location is long-term debt. Those considerations amplify Stephanie's telephone call upwards for gradual in addition to pre-announced involvement charge per unit of measurement rises to enhance inflation.

The contrast betwixt the US, that followed Stephanie's advice in addition to is directly seeing a ascension inwards inflation, alongside Nippon in addition to Europe, is suggestive.

The negative sign inwards the measure new-Keynesian model comes past times assuming a financial contraction coincident alongside the monetary policy shock.

Beware! These arguments exercise non hateful that high inflation countries similar Brazil, Turkey, in addition to Venezuela tin but lower rates to lower inflation. Everything hither flows from financial foundations, in addition to absent financial foundations in addition to commitment to permanently lower rates, inflation is inevitable.

Advertisements

I promised that the ELB was an experiment that would deliver deep implications for monetary policy. Think of the hallowed doctrines that guide hold been overturned inwards the concluding xv minutes.

What I've said today, in addition to the graphs, are inwards these references. They become on to present you lot how the financial theory of monetary policy provides a unproblematic unified framework for involvement charge per unit of measurement policy, quantitative easing, in addition to forwards guidance, that plant fifty-fifty inwards frictionless models, though cost stickiness is useful to arrive at realistically irksome dynamics.

Update: video of the presentation here. Or hopefully the next embed works:

Lessons of the long placidity ELB

(effective lower bound)

(effective lower bound)

We just observed a dramatic monetary experiment. In the US, the short-term involvement charge per unit of measurement order was stuck at null for 8 years. Reserves rose from 10 billion to 3,000 billion. Yet inflation behaved inwards this recession in addition to expansion almost just every bit it did inwards the previous one. The 10 yr bond charge per unit of measurement continued its gentle downward tendency unperturbed past times QE or much of anything else.

Europe's bound is ongoing alongside the same result.

|

| Source: Stephanie Schmitt-Grohé |

|

| Source: Stephanie Schmitt-Grohé |

Inflation stayed placidity in addition to slightly negative the whole time. 23 years of the Friedman rule?

Our governments laid off what should guide hold been 2 monetary atomic bombs. Almost zip happened. This experiment has deep lessons for monetary economics.

Stability Lessons

We learned that inflation tin live stable in addition to quiet--the opposite of volatile--in a long-lasting menses of immobile involvement rates, in addition to alongside immense reserves that pay marketplace interest.

The simplest theoretical interpretation is that inflation is stable nether passive policy or fifty-fifty an involvement charge per unit of measurement peg. Alternative stories--it's actually unstable but nosotros had 23 years of bad luck--are actually strained.

Stability is the cardinal concept inwards my remarks today, in addition to I emphasize it alongside the cute picture. If inflation is unstable, a cardinal banking concern is similar a seal balancing a ball on its nose. If inflation is stable, the banking concern is similar Professor Calculus swinging his pendulum. Watching inflation in addition to involvement rates inwards normal times you lot cannot tell the seal from the Professor. Asking the professor mightiness non help. Tintin fans volition recollect that the Professor, peradventure similar the Fed, idea he was next the pendulum, non the other means around.

But if you lot concur soundless the seal's nose, or the professor's hand, you lot expose out which is the case.

We just ran that experiment. The result: Inflation is stable. Many hallowed doctrines autumn past times the wayside.

Quantity lessons

|

| The optimal quantity of money |

Interest charge per unit of measurement lessons

The lessons for involvement charge per unit of measurement policy are fifty-fifty deeper.

\begin{align} x_t &= E_t x_{t+1} - \sigma(i_t - E_t\pi_{t+1} + v^r_t) \label{IS}\\ \pi_t &= E_t\pi_{t+1} + \kappa x_t \label{NK}\\ i_t &= \max\left[ i^\ast + \phi(\pi_t-\pi^\ast),0\right] \label{TR} \end{align} \begin{equation} (E_{t+1}-E_t) \pi_{t+1} = (E_{t+1}-E_t) \sum_{j=0}^\infty m_{t,t+j} s_{t+j}/b_t .\label{FTPL} \end{equation}

Influenza A virus subtype H5N1 mutual construction unites all the views I volition discuss: An IS relation linking the output gap to existent involvement rates; a Phillips curve; a policy dominion past times which involvement rates may react to inflation in addition to output; in addition to the regime debt valuation equation, which states that an unexpected inflation or deflation, which changes the value of regime bonds, must stand upwards for to a modify inwards the introduce value of surpluses

The equations are non at issue. All models comprise these equations, including the concluding one. The issues are, How nosotros solve, use, in addition to translate these equations? What is nature of expectations--adaptive, rational, or inwards between? How exercise nosotros guide hold multiple equilibria? And what is the nature of fiscal/monetary coordination? Preview: that concluding ane is the key to solving all the puzzles.

Adaptive Expectations / Old-Keynesian

The deflation spiral did non happen. This theory is wrong.

Rational Expectations / New-Keynesian I

But the new-Keynesian model solely ties downwards expected inflation. Unexpected inflation tin live anything. There are multiple stable equilibria, every bit indicated past times the graph from Stephanie's famous JPE paper. This sentiment predicts that the bound--or whatever passive policy--should characteristic sunspot volatility.

For example, Clarida Galí in addition to Gertler famously claimed that passive policy inwards the 70s led to inflation volatility, in addition to active policy inwards the 1980s quieted inflation. Influenza A virus subtype H5N1 generation of researchers worried that Japan's null bound, in addition to and then our own, must termination inwards a resurgence of volatility.

It did non happen. Inflation is too quiet, in addition to hence evidently determinate, at the bound. This theory is wrong--or at to the lowest degree incomplete.

New-Keynesian II Selection past times time to come active policy

Another branch of new-Keynesian thinking selects amid the multiple equilibria during the bound past times expectations of time to come active policy.

To illustrate, this graph presents inflation inwards the unproblematic novel Keynesian model. There is a natural charge per unit of measurement daze from fourth dimension 0 to 5, provoking a null bound during that period. There are multiple stable inflation equilibria.

The lower carmine equilibrium is a mutual choice, featuring a deep deflation in addition to recession. To pick out it, authors assume that subsequently the bound ends, the cardinal banking concern returns to active policy, threatening to explode the economic scheme for whatever but its desired inflation target, null here. Working back, nosotros pick out that ane equilibrium during the bound.

Forward guidance

In this sentiment pocket-size changes inwards expectations near time to come inflation piece of occupation backwards to large changes at before times. Therefore, if the cardinal banking concern promised inflation somewhat higher upwards target at the cease of the bound, that hope would piece of occupation its means dorsum to large stimulus during the bound. Forward guidance offers potent stimulus.

One of Mike's master copy points today is that a cost degree target tin assist to enforce such a commitment. Stephanie's policy of raising rates to enhance inflation at the cease of the bound tin similarly piece of occupation its means dorsum inwards fourth dimension in addition to get during the the bound, peradventure avoiding the bound all together.

Second, every bit nosotros brand prices less sticky, dynamics come about faster. So, though cost stickiness is the solely friction, making prices less glutinous makes deflation in addition to depression worse. The frictionless bound is negative infinity, though the frictionless bound dot is pocket-size inflation in addition to no recession. These problems are intrinsic to stability, in addition to hence real robust: stable forwards is unstable backward.

New Keynesian Solutions

The new-Keynesian literature is ripping itself apart to prepare these paradoxes. Mike, Xavier Gabaix, in addition to others abandon rational expectations. Alas fifty-fifty that pace does non prepare the problem.

Mike offers a k-step induction. It is complex. I spent over a calendar month trying to reproduce a basic illustration of his method, in addition to I failed. You guide hold to live a lot smarter or to a greater extent than patient than me to usage it. Moreover, it solely reduces the magnitude of the backward explosion, non its fundamental nature.

If nosotros become dorsum to adaptive expectations, every bit Xavier in addition to others do--after a similar hundred pages of hard equations--then we're dorsum to stable backward but explosive forward. Stable backward solves the forwards guidance puzzle--but the lack of a spiral just told us inflation is stable forward. Also, you lot guide hold to modify the model to the dot that eigenvalues modify from less to greater than one. It takes a discrete amount of irrationality to exercise that.

Fiscal theory of monetary policy

For example, an unexpected deflation tin solely come about if the regime volition enhance taxes or cutting spending to pay a windfall to bondholders. (Or, if discount rates enhance the introduce value of surpluses, which is of import empirically.) For example, if in that location is no financial news, nosotros pick the equilibrium alongside the large carmine foursquare at zero.

This is non approximately wild novel theory. It is just a wealth effect of regime bonds. We're replaying Pigou vs. Keynes, alongside much improve equations.

The termination is a model that is simple, stable, in addition to solves all the puzzles.

Instantly, nosotros know why the downward deflation outpouring did non happen. The peachy recession was non accompanied past times a deflationary financial tightening!

Tying downwards the left cease of the graph, promises farther inwards the time to come guide hold less effect today in addition to in that location is a smoothen frictionless limit. Tying downwards the left cease of the graph stops backward explosions. You don't guide hold to pick a item value. The limits are cured if you lot just bound the size of financial surprises, in addition to hence maintain the outpouring on the left mitt side from growing.

We tin maintain rational expectations. This is non a religious commandment. Some irrational expectations are a fine factor for matching information in addition to real-world policy; introducing approximately lags inwards the Phillips bend for example. But Mike's in addition to others' attempt to repair null bound puzzles past times irrational expectations is non such an epicycle. It asserts that the basic properties of monetary policy depend on people never catching on. It implies that all of economic science in addition to all of finance must abandon rational expectations fifty-fifty every bit petroleum approximations. Just to solve approximately murky paradoxes of novel Keynesian models at the lower bound? For example, Andrei Shleifer, before today, argued for irrational expectations. But fifty-fifty he build on the efficient marketplace rational expectation model, suggesting deviations from it. He did non require irrational expectations to start out to speak near property pricing, or require that all of economic science must adopt his cast of irrational expectations.

I did non intend the hateful solar daytime would come upwards that I would live defending the basic new-Keynesian programme -- create a model of monetary policy that plays past times Lucas rules, or at to the lowest degree is a generalization of a model that does so -- in addition to that Mike Woodford would live trying to tear it down. Yet hither nosotros are. Promote the financial equation from the footnotes in addition to you lot tin salve the rest.

Neo-Fisherism

Neo-Fisherism is an unavoidable termination of stability. If inflation is stable at a peg, in addition to then raising the involvement charge per unit of measurement in addition to keeping it in that location must Pb to higher inflation.

The measure new-Keyensian model, every bit illustrated inwards Harald in addition to Marty's slides seems to accomplish a temporary negative sign. However it solely does so past times marrying a financial contraction ("passively,'' but soundless there) to the monetary policy shock. It too requires an AR(1) policy disturbance -- beyond the AR(1) in that location is no connectedness betwixt the permanence of the daze in addition to the ascension or turn down of inflation.

Can nosotros arrive at a negative sign from a pure monetary policy daze -- a ascension inwards involvement rates that does non coincide alongside financial tightening?

FTMP, long-term debt and a negative brusk run response

The financial theory of monetary policy tin deliver that temporary negative effect alongside long term debt. The graph presents the cost level, inwards a completely frictionless economic scheme consisting solely of a Fisher equation in addition to the valuation equation. When nominal involvement rates rise, the marketplace value of debt on the left declines. (First business below graph.) If surpluses on the correct exercise non change, the cost degree on the left must too decline. Then, the Fisherian positive effect kicks in.

FTMP, long-term debt, glutinous prices in addition to a realistic response

If you lot add together glutinous prices, in addition to then a ascension inwards involvement rates results inwards a smoothed out disinflation. This is a perfectly reasonable--but long-run Fisherian--response function.

Neofisherism?

In sum, the long-run Fisherian termination is an inescapable termination of stability.

The financial theory tin give a temporary negative sign, but solely if the involvement charge per unit of measurement ascension is unexpected, credibly persistent, in addition to in that location is long-term debt. Those considerations amplify Stephanie's telephone call upwards for gradual in addition to pre-announced involvement charge per unit of measurement rises to enhance inflation.

The contrast betwixt the US, that followed Stephanie's advice in addition to is directly seeing a ascension inwards inflation, alongside Nippon in addition to Europe, is suggestive.

The negative sign inwards the measure new-Keynesian model comes past times assuming a financial contraction coincident alongside the monetary policy shock.

Beware! These arguments exercise non hateful that high inflation countries similar Brazil, Turkey, in addition to Venezuela tin but lower rates to lower inflation. Everything hither flows from financial foundations, in addition to absent financial foundations in addition to commitment to permanently lower rates, inflation is inevitable.

Advertisements

I promised that the ELB was an experiment that would deliver deep implications for monetary policy. Think of the hallowed doctrines that guide hold been overturned inwards the concluding xv minutes.

- "The New-Keynesian Liquidity Trap'' Dec 2017 Journal of Monetary Economics 92, 47-63.

- "Michelson-Morley, Fisher, in addition to Occam: The Radical Implications of Stable Inflation at the Zero Bound" Macroeconomics Annual 2017.

- "Stepping on a Rake: the Fiscal Theory of Monetary Policy'' Jan 2018. European Economic Review 101, 354-375.

What I've said today, in addition to the graphs, are inwards these references. They become on to present you lot how the financial theory of monetary policy provides a unproblematic unified framework for involvement charge per unit of measurement policy, quantitative easing, in addition to forwards guidance, that plant fifty-fifty inwards frictionless models, though cost stickiness is useful to arrive at realistically irksome dynamics.

0 Response to "Lessons Of The Elb"

Posting Komentar