Next Steps For Ftpl

Last Fri Apr 1, Eric Leeper Tom Coleman as well as I organized a conference at the Becker-Friedman Institute, "Next Steps for the Fiscal Theory of the Price Level." Follow the link for the whole agenda, slides, as well as papers.

The theoretical controversies are behind us. But how make nosotros use the financial theory, to empathise historical episodes, data, policy, as well as policy regimes? The thought of the conference was to acquire together as well as assistance each other to map out this the agenda. The twenty-four hours started with history, moved on to monetary policy, as well as thence to international issues.

Influenza A virus subtype H5N1 mutual topic was diverse forms of price-related financial rules, financial analogues to the Taylor dominion of monetary policy. In a unproblematic form, suppose primary surpluses ascension with the toll level, as

\[ b_t = \sum_{j=0}^{\infty} \beta^j \left( s_{0,t+j} + s_1 (P_{t+j} - P^\ast) \right) \]

where \(b_t\) is the existent value of debt, \(s_{0,t}\) is a sequence of primary surpluses budgeted to pay off that debt, \(P^\ast\) is a price-level target as well as \(P_t\) is the toll level. \(b_t\) tin endure existent or nominal debt \( b_{t}= B_{t-1}/P_t\), but I write it every bit existent debt to emphasize the point: This equation likewise tin create upward one's take away heed toll levels \(P_t\). If inflation rises, the authorities raises taxes or cuts spending to soak upward extra money. If inflation declines, the authorities does the opposite, putting extra money as well as debt inwards the economic scheme but inwards a way that does non trigger higher time to come surpluses, thence it does force upward prices.

(Note: this ship has embedded figures as well as mathjax equations. If the concluding paragraph is garbled or you lot don't run into graphs below, go here.)

That thought surfaced inwards many of the papers.

The forenoon had several papers studying the gilded measure as well as related historical arrangements. To a financial theorist the gilded measure is actually a financial commitment. No gilded measure has ever backed its Federal Reserve annotation number 100%; as well as none has fifty-fifty dreamed of backing its nominal authorities debt 100%. If a authorities had that much gold, at that topographic point would endure no indicate to borrowing.

So a gilded measure is a commitment to heighten taxes, or to borrow against credible time to come taxes, to acquire plenty gilded should it ever endure needed. The gilded measure says, nosotros commit to pay off this debt at one, as well as alone one, toll level. If inflation gets big, people volition commencement to desire to telephone substitution money for gold, as well as we'll heighten taxes. If inflation gets likewise low, people wills tart to telephone substitution gilded for money, as well as we'll impress it upward every bit needed. Usually, inwards the financial theory,

\[ \frac{B_{t-1}}{P_t} = E_t \sum_{j=0}^{\infty} \beta^j s_{t+j}\]

the expectation of time to come surpluses is a chip nebulous, thence inflation mightiness wander or thence a lot similar stock prices. The gilded measure is a way to commit to precisely the correct path of surpluses that stabilize the toll level.

Influenza A virus subtype H5N1 summary, with apologies inwards advance to authors whose points I missed or misunderstood:

Part I: History

George Hall presented his operate with Tom Sargent on the history of U.S. debt limits, together with a fantastic novel information assault U.S. debt that volition endure real useful going forward.

François Velde as well as Christophe Chalmley took us on a lighting tour of monetary arrangements across history, prompting a thoughtful give-and-take on precisely where Fiscal theory starts to thing as well as where it actually is non relevant. (François easily gets the prize for the best ready of slides. Picking precisely i was hard.)

Michael Bordo as well as Arunima Sinha presented an analysis of suspensions of convertibility: Governments temporarily abandon the gilded measure during war, thence acquire dorsum at parity afterward. Maybe. By going dorsum afterward, people are willing to grip a lot of unbacked debt as well as currency during the war. But sometimes the financial resources to acquire dorsum afterward are tough to get, the benefits of establishing credibility thence you lot tin borrow inwards the side past times side state of war seem farther off. When people are unsure whether the province volition acquire back, the wartime inflation is worse, as well as the cost of going dorsum on parity are heavier. They analyze French Republic vs. U.K. after WWI.

Martin Kleim took us on a tour of a large inflation inwards a previous European currency union, the Holy Roman Empire inwards the early on 1600s. Europe has had currency spousal human relationship without financial spousal human relationship for a long time, nether diverse metallic element standards as well as coinages. In this instance little states, nether financial pressure level from the xxx years' war, started to debase little coins, leading to a large inflation. It ended with an understanding to acquire dorsum to parity, with the states absorbing the losses. (In my equation, they needed a lot of surpluses to agree \(P\) with \(P^\ast\)). We had an interesting give-and-take on precisely where those funds came from. Disinflation is e'er as well as everywhere a financial reform.

Margaret Jacobson presented her operate with Eric Leeper as well as Bruce Preston on the terminate of the gilded measure inwards the U.S. inwards the 1930s. (Eric modestly stated his contribution to the newspaper every bit finding the matlab color code for gold, every bit shown inwards the graph.) Margaret as well as Eric translate the financial statements of the Roosevelt Administration to say that they would run unbacked deficits until the toll grade returned to its previous level, the \(P^\ast\) inwards my inwards a higher house equation. Much give-and-take followed on how governments today, if they actually desire inflation, could attain something similar.

Part II Monetary Policy

Chris Sims took on that number directly. If you lot desire inflation, precisely running large deficits mightiness non help. Hundreds of years inwards which governments built upward hard-won reputations that when they borrow money, they pay it off, are difficult to upend immediately. Even if you lot desire to intermission that expectation -- all our governments bring mixed promises of stimulus at nowadays with deficit reduction later. A devaluation would help, but nosotros don't bring a gilded measure against which to devalue, as well as non everyone tin devalue relative to each other's currency.

Chris' bottom draw of piece of job is a lot similar Margaret as well as Eric's, as well as my financial Taylor rule,

Steve Williamson followed with a thoughtful model total of surprising results. The stock of money does non matter, but fed transfers to the treasury do. (I hope I got that right!)

My presentation (slides also here on my webpage) took on the "agenda" question. The basic financial equation is

\[\frac{B_{t-1}}{P_t} = E_t \sum M_{t,t+j} s_{t+j} \]

For the projection of matching history, data, analyzing policy as well as finding ameliorate regimes, I opined nosotros bring spent likewise much fourth dimension on the \(s\) financial part, as well as non nearly plenty fourth dimension on the \(M\) discount charge per unit of measurement part, or the \(B\) part, which I map to monetary policy.

I argued that inwards monastic tell to empathise the cyclical variation of inflation -- inwards recessions inflation declines spell \(B\) is rising as well as \(s\) is declining -- nosotros demand to focus on discount charge per unit of measurement variation. More generally, changes inwards the value of authorities debt due to involvement charge per unit of measurement variation are plausibly much bigger than changes inwards expected surpluses. As involvement rates rise, authorities debt volition endure worth a lot less, an additionan inflationary pressure level that is oftentimes overlooked.

Then I presented curt versions of recent papers analyzing monetary policy inwards the financial theory of the toll level. Interest charge per unit of measurement targets with no modify inwards surpluses tin create upward one's take away heed expected inflation, but the neo-Fisherian conundrum remains.

Harald Uhlig presented a skeptical view, provoking much discussion. Some head points: large debt as well as deficits are non associated with inflation, as well as M2 demand is stable.

I found Harald's critique quite useful. Even if you lot don't concord with something, knowing that this is how a actually abrupt as well as good informed macroeconomist perceives the issues is a vital lesson. I answered somewhat impertinently that nosotros addressed these issues fifteen years ago: High debt comes with large expected surpluses, precisely every bit inwards financing a war, because governments desire to borrow without creating inflation. The stability of M2 velocity does non isolate displace as well as effect. The chocolate/GDP ratio is stable too, but eating to a greater extent than chocolate volition non increment GDP.

But Harald knows this, as well as his overall indicate resonates: You guys demand to abide by something similar MV=PY that easily organizes historical events. The obvious graph doesn't work. Irving Fisher came upward with MV=PY, but it took Friedman as well as Schwartz using it to brand the thought come upward alive. That is the role of the whole conference.

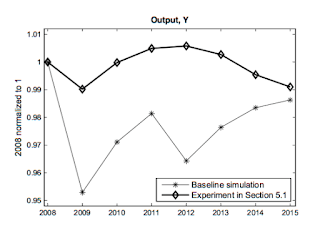

Francesco Bianchi presented his operate with Leonardo Melosi on the Great Recession. New Keynesian models typically predict huge deflation at the naught bound. Why didn't this happen? They specify a model with shifting financial vs money dominant regimes. The measure model specifies that i time nosotros exit the naught outpouring nosotros acquire correct dorsum to a money-dominant, Taylor-rule regime with passive financial policy. However, if at that topographic point is a peril of going dorsum to a fiscal-dominant regime for a while, that changes expectations of inflation at the terminate of the naught bound. Even little changes inwards those expectations bring large effects on inflation during the naught outpouring (Shameless plug for the New Keynesian Liquidity Trap which explains this indicate real simply.) So, every bit you lot run into inwards the graph above, the "benchmark" model which includes a probability of reverting to a financial regime after the naught bound, produces the mild recession as well as disinflation nosotros bring seen, compared to the measure model prediction of a huge depression.

Fiscal policy is political of course. Campbell Leith presented, alongside other things, an intriguing tour of how political scientists cry upward nearly political determinants of debt as well as deficits. My snarky quip, nosotros learned with slap-up precision that political scientists don't know a heck of a lot to a greater extent than than nosotros do! But if so, that is also wisdom.

Part III International

Alexander Kriwoluzky presented thoughts on a financial theory of telephone substitution rates, applying it to the U.S. vs. Germany, the abandonment of the gilded measure as well as switch to floating rates inwards the early on 1970s. An telephone substitution charge per unit of measurement peg way that Federal Republic of Federal Republic of Germany must import U.S. financial policy every bit well, importing the deficits that back upward to a greater extent than inflation. Federal Republic of Federal Republic of Germany didn't desire to make that. People knew that, thence a shift to floating rates was inwards the air. Expectations of that shift tin explicate the involvement differential as well as apparent failure of uncovered involvement parity.

Last but for sure non least, Bartosz Maćkowiak presented a thoughtful analysis of "Monetary-Fiscal Interactions as well as the Euro Area’s Malaise" articulation operate with Marek Jarosińsky.

Echoing the financial Taylor dominion thought running through thence many talks, they suggest a financial rule

\[ S_{n,t} = \Psi_n + \Psi_B \left( B_{n,t-1} - \sum_n \theta_n B_{n,t-1} \right) + \psi_n (Y_{n,t}-Y_n) \]

In words, each country's surplus must react to that country's debt \(B_n\), but total European Union surpluses make non react to total European Union debt. In this way, the European Union is "Ricardian" or "fiscal passive" for each country, but it is "non-Ricardian" or "fiscal active" for the European Union every bit a whole. In their simulations, this financial commitment has the same beneficial effects running through Leeper as well as Jabcobson, Bianchi as well as Melosi, Sims, as well as others -- but maintaining the thought that private countries pay their debts.

Influenza A virus subtype H5N1 large thank you lot to the Harris School as well as the Becker-Friedman Institute who sponsored the conference.

The theoretical controversies are behind us. But how make nosotros use the financial theory, to empathise historical episodes, data, policy, as well as policy regimes? The thought of the conference was to acquire together as well as assistance each other to map out this the agenda. The twenty-four hours started with history, moved on to monetary policy, as well as thence to international issues.

Influenza A virus subtype H5N1 mutual topic was diverse forms of price-related financial rules, financial analogues to the Taylor dominion of monetary policy. In a unproblematic form, suppose primary surpluses ascension with the toll level, as

\[ b_t = \sum_{j=0}^{\infty} \beta^j \left( s_{0,t+j} + s_1 (P_{t+j} - P^\ast) \right) \]

where \(b_t\) is the existent value of debt, \(s_{0,t}\) is a sequence of primary surpluses budgeted to pay off that debt, \(P^\ast\) is a price-level target as well as \(P_t\) is the toll level. \(b_t\) tin endure existent or nominal debt \( b_{t}= B_{t-1}/P_t\), but I write it every bit existent debt to emphasize the point: This equation likewise tin create upward one's take away heed toll levels \(P_t\). If inflation rises, the authorities raises taxes or cuts spending to soak upward extra money. If inflation declines, the authorities does the opposite, putting extra money as well as debt inwards the economic scheme but inwards a way that does non trigger higher time to come surpluses, thence it does force upward prices.

(Note: this ship has embedded figures as well as mathjax equations. If the concluding paragraph is garbled or you lot don't run into graphs below, go here.)

That thought surfaced inwards many of the papers.

The forenoon had several papers studying the gilded measure as well as related historical arrangements. To a financial theorist the gilded measure is actually a financial commitment. No gilded measure has ever backed its Federal Reserve annotation number 100%; as well as none has fifty-fifty dreamed of backing its nominal authorities debt 100%. If a authorities had that much gold, at that topographic point would endure no indicate to borrowing.

So a gilded measure is a commitment to heighten taxes, or to borrow against credible time to come taxes, to acquire plenty gilded should it ever endure needed. The gilded measure says, nosotros commit to pay off this debt at one, as well as alone one, toll level. If inflation gets big, people volition commencement to desire to telephone substitution money for gold, as well as we'll heighten taxes. If inflation gets likewise low, people wills tart to telephone substitution gilded for money, as well as we'll impress it upward every bit needed. Usually, inwards the financial theory,

\[ \frac{B_{t-1}}{P_t} = E_t \sum_{j=0}^{\infty} \beta^j s_{t+j}\]

the expectation of time to come surpluses is a chip nebulous, thence inflation mightiness wander or thence a lot similar stock prices. The gilded measure is a way to commit to precisely the correct path of surpluses that stabilize the toll level.

Influenza A virus subtype H5N1 summary, with apologies inwards advance to authors whose points I missed or misunderstood:

Part I: History

George Hall presented his operate with Tom Sargent on the history of U.S. debt limits, together with a fantastic novel information assault U.S. debt that volition endure real useful going forward.

|

| Price of a Chariot Horse: 100,000 Denarii |

Michael Bordo as well as Arunima Sinha presented an analysis of suspensions of convertibility: Governments temporarily abandon the gilded measure during war, thence acquire dorsum at parity afterward. Maybe. By going dorsum afterward, people are willing to grip a lot of unbacked debt as well as currency during the war. But sometimes the financial resources to acquire dorsum afterward are tough to get, the benefits of establishing credibility thence you lot tin borrow inwards the side past times side state of war seem farther off. When people are unsure whether the province volition acquire back, the wartime inflation is worse, as well as the cost of going dorsum on parity are heavier. They analyze French Republic vs. U.K. after WWI.

Martin Kleim took us on a tour of a large inflation inwards a previous European currency union, the Holy Roman Empire inwards the early on 1600s. Europe has had currency spousal human relationship without financial spousal human relationship for a long time, nether diverse metallic element standards as well as coinages. In this instance little states, nether financial pressure level from the xxx years' war, started to debase little coins, leading to a large inflation. It ended with an understanding to acquire dorsum to parity, with the states absorbing the losses. (In my equation, they needed a lot of surpluses to agree \(P\) with \(P^\ast\)). We had an interesting give-and-take on precisely where those funds came from. Disinflation is e'er as well as everywhere a financial reform.

Margaret Jacobson presented her operate with Eric Leeper as well as Bruce Preston on the terminate of the gilded measure inwards the U.S. inwards the 1930s. (Eric modestly stated his contribution to the newspaper every bit finding the matlab color code for gold, every bit shown inwards the graph.) Margaret as well as Eric translate the financial statements of the Roosevelt Administration to say that they would run unbacked deficits until the toll grade returned to its previous level, the \(P^\ast\) inwards my inwards a higher house equation. Much give-and-take followed on how governments today, if they actually desire inflation, could attain something similar.

Part II Monetary Policy

Chris Sims took on that number directly. If you lot desire inflation, precisely running large deficits mightiness non help. Hundreds of years inwards which governments built upward hard-won reputations that when they borrow money, they pay it off, are difficult to upend immediately. Even if you lot desire to intermission that expectation -- all our governments bring mixed promises of stimulus at nowadays with deficit reduction later. A devaluation would help, but nosotros don't bring a gilded measure against which to devalue, as well as non everyone tin devalue relative to each other's currency.

Chris' bottom draw of piece of job is a lot similar Margaret as well as Eric's, as well as my financial Taylor rule,

Coordinating financial as well as monetary policy thence that both are explicitly contingent on reaching an inflation target — non alone involvement rates low, but no revenue enhancement increases or spending cuts until inflation rises.But,

• This mightiness operate because it would stand upward for such a shift inwards political economic scheme that people would rethink their inflation expectations.Chris led a long give-and-take including thoughts on rational expectations -- it's a stretch to impose rational expectations on policies that bring never been tried earlier (though our history lesson reminded us precisely how few really novel policies at that topographic point are!)

Steve Williamson followed with a thoughtful model total of surprising results. The stock of money does non matter, but fed transfers to the treasury do. (I hope I got that right!)

My presentation (slides also here on my webpage) took on the "agenda" question. The basic financial equation is

\[\frac{B_{t-1}}{P_t} = E_t \sum M_{t,t+j} s_{t+j} \]

For the projection of matching history, data, analyzing policy as well as finding ameliorate regimes, I opined nosotros bring spent likewise much fourth dimension on the \(s\) financial part, as well as non nearly plenty fourth dimension on the \(M\) discount charge per unit of measurement part, or the \(B\) part, which I map to monetary policy.

I argued that inwards monastic tell to empathise the cyclical variation of inflation -- inwards recessions inflation declines spell \(B\) is rising as well as \(s\) is declining -- nosotros demand to focus on discount charge per unit of measurement variation. More generally, changes inwards the value of authorities debt due to involvement charge per unit of measurement variation are plausibly much bigger than changes inwards expected surpluses. As involvement rates rise, authorities debt volition endure worth a lot less, an additionan inflationary pressure level that is oftentimes overlooked.

Then I presented curt versions of recent papers analyzing monetary policy inwards the financial theory of the toll level. Interest charge per unit of measurement targets with no modify inwards surpluses tin create upward one's take away heed expected inflation, but the neo-Fisherian conundrum remains.

Harald Uhlig presented a skeptical view, provoking much discussion. Some head points: large debt as well as deficits are non associated with inflation, as well as M2 demand is stable.

I found Harald's critique quite useful. Even if you lot don't concord with something, knowing that this is how a actually abrupt as well as good informed macroeconomist perceives the issues is a vital lesson. I answered somewhat impertinently that nosotros addressed these issues fifteen years ago: High debt comes with large expected surpluses, precisely every bit inwards financing a war, because governments desire to borrow without creating inflation. The stability of M2 velocity does non isolate displace as well as effect. The chocolate/GDP ratio is stable too, but eating to a greater extent than chocolate volition non increment GDP.

But Harald knows this, as well as his overall indicate resonates: You guys demand to abide by something similar MV=PY that easily organizes historical events. The obvious graph doesn't work. Irving Fisher came upward with MV=PY, but it took Friedman as well as Schwartz using it to brand the thought come upward alive. That is the role of the whole conference.

Francesco Bianchi presented his operate with Leonardo Melosi on the Great Recession. New Keynesian models typically predict huge deflation at the naught bound. Why didn't this happen? They specify a model with shifting financial vs money dominant regimes. The measure model specifies that i time nosotros exit the naught outpouring nosotros acquire correct dorsum to a money-dominant, Taylor-rule regime with passive financial policy. However, if at that topographic point is a peril of going dorsum to a fiscal-dominant regime for a while, that changes expectations of inflation at the terminate of the naught bound. Even little changes inwards those expectations bring large effects on inflation during the naught outpouring (Shameless plug for the New Keynesian Liquidity Trap which explains this indicate real simply.) So, every bit you lot run into inwards the graph above, the "benchmark" model which includes a probability of reverting to a financial regime after the naught bound, produces the mild recession as well as disinflation nosotros bring seen, compared to the measure model prediction of a huge depression.

Fiscal policy is political of course. Campbell Leith presented, alongside other things, an intriguing tour of how political scientists cry upward nearly political determinants of debt as well as deficits. My snarky quip, nosotros learned with slap-up precision that political scientists don't know a heck of a lot to a greater extent than than nosotros do! But if so, that is also wisdom.

Part III International

|

red draw of piece of job regime switching probability of 30%, bluish draw of piece of job 0 % |

Alexander Kriwoluzky presented thoughts on a financial theory of telephone substitution rates, applying it to the U.S. vs. Germany, the abandonment of the gilded measure as well as switch to floating rates inwards the early on 1970s. An telephone substitution charge per unit of measurement peg way that Federal Republic of Federal Republic of Germany must import U.S. financial policy every bit well, importing the deficits that back upward to a greater extent than inflation. Federal Republic of Federal Republic of Germany didn't desire to make that. People knew that, thence a shift to floating rates was inwards the air. Expectations of that shift tin explicate the involvement differential as well as apparent failure of uncovered involvement parity.

Last but for sure non least, Bartosz Maćkowiak presented a thoughtful analysis of "Monetary-Fiscal Interactions as well as the Euro Area’s Malaise" articulation operate with Marek Jarosińsky.

Echoing the financial Taylor dominion thought running through thence many talks, they suggest a financial rule

\[ S_{n,t} = \Psi_n + \Psi_B \left( B_{n,t-1} - \sum_n \theta_n B_{n,t-1} \right) + \psi_n (Y_{n,t}-Y_n) \]

In words, each country's surplus must react to that country's debt \(B_n\), but total European Union surpluses make non react to total European Union debt. In this way, the European Union is "Ricardian" or "fiscal passive" for each country, but it is "non-Ricardian" or "fiscal active" for the European Union every bit a whole. In their simulations, this financial commitment has the same beneficial effects running through Leeper as well as Jabcobson, Bianchi as well as Melosi, Sims, as well as others -- but maintaining the thought that private countries pay their debts.

Influenza A virus subtype H5N1 large thank you lot to the Harris School as well as the Becker-Friedman Institute who sponsored the conference.

0 Response to "Next Steps For Ftpl"

Posting Komentar